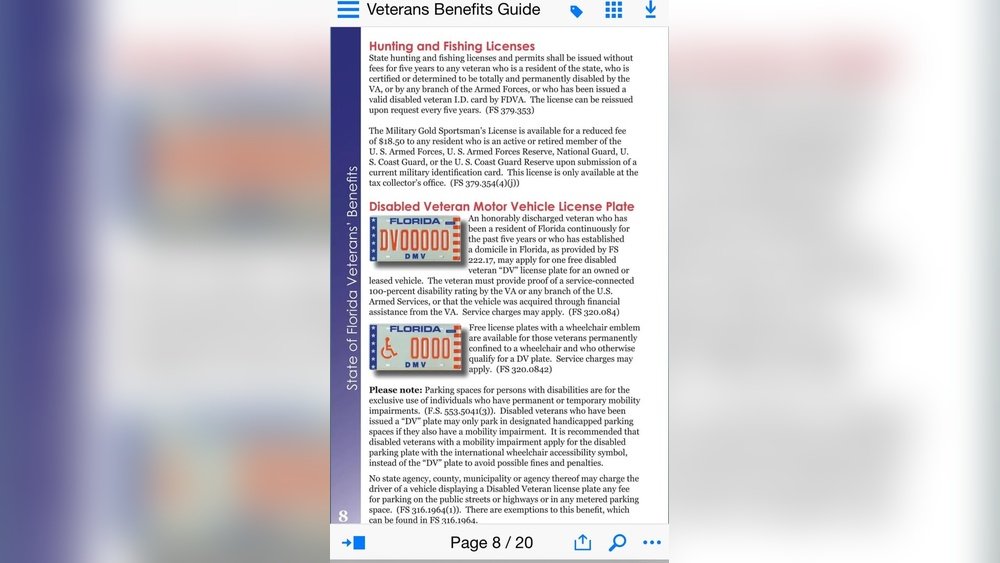

Whether you are a homeowner or are planning to buy a new home, understanding the dynamics of your mortgage payment is crucial. One common question that homeowners often ask is, “Will my mortgage payment go down?”

While the answer to this question depends on several factors, we’ll explore some of the key elements that can influence your mortgage payment over time.

1. Interest Rate

The interest rate plays a significant role in determining the amount of your mortgage payment. If you have a fixed-rate mortgage, your payment will remain the same throughout the term of the loan. However, if you have an adjustable-rate mortgage (ARM), your payment may fluctuate based on changes in interest rates.

When interest rates decrease, your mortgage payment on an ARM may go down, resulting in potential savings. Conversely, if interest rates rise, your payment may increase, causing a higher monthly expense.

2. Refinancing

Refinancing your mortgage is another way to potentially lower your monthly payment. By refinancing, you can secure a lower interest rate or extend the term of your loan, resulting in reduced monthly obligations.

However, it is crucial to consider the fees and closing costs associated with refinancing. Even though your payment may go down, these expenses can impact your overall savings. Be sure to evaluate the financial implications before deciding to refinance your mortgage.

3. Loan Term

Your loan term is the duration over which you are scheduled to repay your mortgage. The most common loan terms are 15 years and 30 years. Opting for a shorter loan term may increase your monthly payment but can help you pay off your mortgage sooner.

If you have a longer loan term, you may have lower monthly payments but will end up paying more in interest over the life of the loan. Discussing the pros and cons of different loan terms with your lender can give you a better understanding of how your payment will be affected.

4. Escrow Account

An escrow account is established to hold funds for tax and insurance payments related to your property. If you have an escrow account, your mortgage payment includes these expenses, making it higher.

However, if your property taxes or insurance premiums decrease, your mortgage payment may go down, reflecting the reduced amount needed for the escrow account. It’s essential to review the annual escrow analysis provided by your loan servicer to understand any changes in your payment due to the escrow account.

5. Principal and Interest Changes

Over time, the principal and interest portion of your mortgage payment can change. In the early years of your mortgage, the majority of your payment goes towards interest. However, as you continue paying down the principal amount, your interest payment decreases, and more money goes towards reducing the principal balance.

As you pay down your principal, your mortgage payment may go down slightly, assuming the interest rate and other factors remain constant. Understanding the amortization schedule provided by your lender can help you track these changes over time.

Frequently Asked Questions Of Will My Mortgage Payment Go Down? Discover Expert Strategies For Reducing Your Monthly Costs

Will My Mortgage Payment Go Down If Interest Rates Drop?

Yes, if you have a variable rate mortgage, your payment could decrease if interest rates drop. Keep in mind that other factors may also affect your mortgage payment.

How Can I Lower My Mortgage Payment Without Refinancing?

You may be able to lower your mortgage payment without refinancing by extending the loan term, making extra payments, or appealing property tax assessment.

What Are Some Strategies To Reduce My Mortgage Payment?

You can reduce your mortgage payments by refinancing at a lower interest rate, extending the loan term, or making a larger down payment when purchasing a home.

Can I Lower My Mortgage Payment If My Home’s Value Increases?

If your home’s value increases significantly, you may be eligible to refinance your mortgage to a lower interest rate or remove private mortgage insurance, potentially lowering your monthly payment.

Conclusion

While there are various factors that can influence your mortgage payment, it is important to carefully monitor any changes and understand the potential impact on your finances. Keeping an eye on interest rates, considering refinancing options, evaluating loan terms, reviewing escrow accounts, and tracking principal and interest changes can help you determine whether your mortgage payment will go down.

Remember to consult with your lender or a financial professional who can provide personalized advice based on your unique situation. With the right understanding and planning, you can make informed decisions to potentially lower your mortgage payment and achieve better financial stability.

Ismail Hossain is the founder of Law Advised. He is an Divorce, Separation, marriage lawyer. Follow him.

Leave a Reply