Are you facing pressure from debt collectors in California? Understanding your rights under the state’s credit collection laws can make all the difference.

These laws are designed to protect you from unfair practices and set clear limits on how debt can be collected. But do you know exactly how long a debt can be pursued, what methods collectors can legally use, or what recent changes might affect you?

This article breaks down everything you need to know about credit collection laws in California, so you can confidently handle debt issues without feeling overwhelmed or taken advantage of. Keep reading to empower yourself with the knowledge that could save you time, stress, and money.

Credit: www.fullmanfirm.com

California Debt Collection Limits

California sets clear limits on how long debt collectors can pursue debts. These rules protect consumers from old debts suddenly becoming collectible. Understanding these limits helps you know your rights and options.

Debt collection limits depend on the type of debt and specific actions taken by the debtor. The law specifies how long a creditor has to file a lawsuit. Knowing these details can prevent unfair collection attempts.

Statute Of Limitations For Debt

The statute of limitations is the deadline for legal action to collect debt. In California, this limit is usually four years. The countdown starts from the date of the last activity on the debt. After this period, courts will likely dismiss a collection lawsuit.

Types Of Debts Covered

These limits apply to many types of debts. Written contracts, credit card debts, and promissory notes fall under this rule. Some debts, like unpaid rent or oral agreements, may have shorter limits. Each debt type has its own specific time frame.

Effect Of Last Payment On Deadlines

The last payment or written acknowledgment resets the clock. This means the four-year limit starts anew from that date. Even a small payment can extend the collection period. Consumers should be careful when making payments on old debts.

Credit: www.youtube.com

Consumer Protections Against Debt Collectors

Consumers in California receive strong protections against aggressive debt collectors. These laws limit what debt collectors can do and protect your rights. Knowing these protections helps you handle debt collection calls with confidence.

California laws focus on fair treatment and stopping harassment. They also give you clear rights during the collection process. Understanding these rules can prevent abuse and confusion.

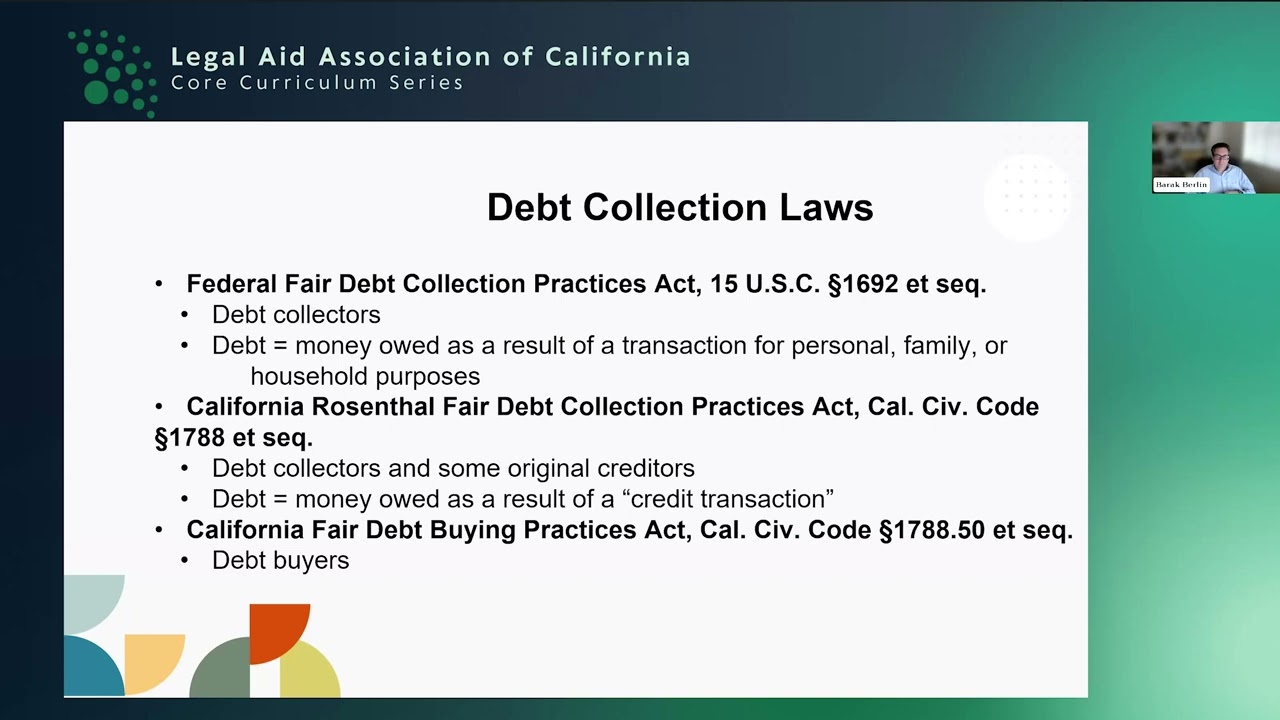

Rosenthal Fair Debt Collection Practices Act

This state law controls how debt collectors operate in California. It builds on federal rules but adds more protections. Collectors must act honestly and avoid unfair methods. They cannot use threats, lies, or misleading statements.

The Rosenthal Act applies to anyone trying to collect consumer debts. It covers phone calls, letters, and other contacts. Violations of this law can lead to legal penalties for collectors.

Prohibited Debt Collection Tactics

Collectors cannot call at odd hours or contact you repeatedly. They must stop if you request no contact in writing. Using abusive language or threats is illegal. Collectors cannot share your debt information with others.

They also cannot pretend to be lawyers or government officials. False statements about the amount owed or legal consequences are banned. These rules protect your privacy and peace of mind.

Rights When Contacted By Collectors

You have the right to request debt validation within 30 days. Collectors must provide proof of the debt if asked. You can ask collectors to stop contacting you. They must then stop except to notify about legal actions.

Consumers may dispute debts if they believe errors exist. Collectors must investigate and correct mistakes. Knowing these rights helps you avoid scams and unfair demands.

New California Debt Collection Laws

California has introduced new debt collection laws to protect consumers and businesses. These laws aim to create fairer practices in collecting debts. They set clear rules for debt collectors and debtors. Understanding these changes is crucial for anyone dealing with debt collection in California.

Recent Legislative Changes

California passed new laws to regulate debt collection more strictly. The laws limit the ways collectors contact debtors. They also set stricter rules on what collectors can say or do. The statute of limitations for filing debt lawsuits remains four years. New laws also address unfair or deceptive practices by collectors.

Impact On Commercial Debt Collection

Commercial debt collection now faces tighter regulations. Debt collectors must follow new procedures before suing businesses for debt. Collectors need proper documentation to prove commercial debt. These laws aim to reduce wrongful or aggressive collection efforts. Businesses gain better protection against unfair debt collection tactics.

Enforcement And Compliance Requirements

Debt collectors must comply with new rules to avoid penalties. The California Department of Financial Protection and Innovation enforces these laws. Collectors must train staff on updated rules and maintain compliance records. Violating the laws can lead to fines and legal action. Clear compliance helps collectors build trust and avoid disputes.

Credit: www.youtube.com

Dealing With Debt Collection Agencies

Dealing with debt collection agencies in California requires knowing your rights and the law. These agencies contact you to collect money owed on debts. Understanding the rules helps protect you from unfair practices. California has specific laws that regulate how these agencies operate.

Knowing the right steps to take can reduce stress and prevent mistakes. Always verify the legitimacy of the collector before paying any debt. Report any unfair or illegal behavior to the proper authorities. This section explains what to do when a collection agency contacts you.

How To Verify A Debt Collector’s License

California requires debt collectors to hold a valid license. You can check this license online through the California Department of Financial Protection and Innovation (DFPI). Verify the collector’s name and license number to ensure they are authorized. Never share personal information until you confirm their legitimacy. This simple step protects you from scams and fraud.

Steps Before Paying A Collection Agency

Request a written notice of the debt from the collector. This must include the amount owed and the creditor’s name. Review your records to confirm the debt is yours. Check the statute of limitations; California usually limits debt collection lawsuits to four years. Do not rush to pay; ask for a payment plan if needed. Keep records of all communications and payments for your protection.

Reporting Unfair Practices

Debt collectors must follow fair debt collection laws in California. They cannot use threats, harassment, or false statements. If you experience unfair practices, file a complaint with the DFPI. You can also contact the Federal Trade Commission (FTC) for help. Reporting these actions helps stop abusive collectors and protects others.

Federal Vs California Debt Collection Rules

Understanding the differences between federal and California debt collection rules is crucial. Both sets of laws protect consumers but vary in scope and details. Federal laws set a baseline, while California laws often provide stronger safeguards. These distinctions affect how debt collectors must operate within the state. Knowing the differences helps consumers recognize their rights and spot illegal practices.

Differences In Definitions Of Debt Collectors

The federal law defines debt collectors broadly, including third-party collectors and agencies. California’s law has a wider definition. It covers original creditors who collect their own debts if they use unfair methods. This means more entities must follow strict rules in California. The broader definition offers consumers more protection against harassment and abuse.

Federal Fair Debt Collection Practices Act Overview

The Fair Debt Collection Practices Act (FDCPA) is the main federal law on debt collection. It limits how debt collectors can contact debtors. The FDCPA bans threats, harassment, and false statements. It requires collectors to identify themselves and provide verification of debts. This law applies nationwide and sets minimum standards to protect consumers.

How State Laws Offer Additional Protections

California’s debt collection laws add extra layers of protection beyond federal rules. The state law sets stricter limits on calls and letters. It also requires clear disclosure of debt collector identity. California bans certain aggressive tactics allowed under federal law. The state law provides longer statutes of limitations for debt collection lawsuits. These measures give Californians stronger defenses against unfair debt collection.

Frequently Asked Questions

What Is The New Law For Debt Collection In California?

The new California law limits debt collection lawsuits to four years from the last payment. It prohibits unfair and deceptive practices by collectors. Debt collectors must follow stricter rules to protect consumers’ rights and provide clear communication during collection attempts.

How Long Before A Debt Becomes Uncollectible In California?

In California, most debts become uncollectible after four years from the debtor’s last payment. This is the statute of limitations. Credit card and written contract debts follow this four-year rule for filing lawsuits. After this period, creditors usually cannot legally enforce collection through court.

What Is The 7 7 7 Rule For Debt Collectors?

The 7 7 7 rule limits debt collectors to three calls a week, between 7 a. m. and 7 p. m. , for up to seven weeks.

What Is Trump’s New Law About Debt Collectors?

Trump’s new law limits aggressive tactics by debt collectors and requires clearer communication with consumers. It strengthens consumer protections.

What Is The Statute Of Limitations For Debt In California?

In California, the statute of limitations is generally four years. This period starts from the last payment or written agreement date. After this time, collectors cannot sue to collect the debt.

Conclusion

Understanding California’s credit collection laws helps protect your rights. Debt collectors must follow specific rules and cannot harass or deceive you. Laws limit how long they can sue to collect a debt, usually four years. Knowing these rules helps you respond wisely to collection efforts.

Stay informed to avoid unfair practices and manage your debt better.

Ismail Hossain is the founder of Law Advised. He is an Divorce, Separation, marriage lawyer. Follow him.

Leave a Reply